If you're a real estate investor in Texas, you’ve probably heard the buzz about DSCR loans. Whether you’re new to the game or leveling up your investment portfolio, understanding the DSCR loan process can mean the difference between a smooth closing and a stressful slog. At Casey Sullivan Mortgage, we’re all about making things clear, friendly, and tailored just for you. So, let’s walk through a simple, step-by-step checklist for getting a DSCR loan in Texas, and set you up for investing success—without the headaches.

What’s a DSCR Loan, Anyway?

Before we get into the nitty-gritty, let’s demystify DSCR loans. DSCR stands for Debt Service Coverage Ratio. In plain English, it’s a fancy way lenders measure if your rental property's income will cover its loan payments. Unlike traditional mortgages, DSCR loans don’t focus on your personal income—they look at the property’s cash flow instead.

This is a game-changer for investors, especially if you own multiple properties or have income that’s tough to document. If your rental can pay for itself (and then some), you’re in good shape for a DSCR loan.

Pro tip: DSCR loans are ideal if you want to build a real estate portfolio without jumping through endless hoops about your W-2s or tax returns.

Getting Ready: What Lenders Want to See

Preparation is half the battle. When you’re eyeing a DSCR loan, you’ll want to gather the right paperwork and details ahead of time. Lenders—like us at Casey Sullivan Mortgage—will want to see proof that your property is a solid investment.

Here’s what you’ll typically need:

- Property details: Purchase contract, address, and description

- Estimated rental income: Lease agreements or market rent analysis

- Down payment funds: Bank statements showing you have the cash

- Credit report: DSCR loans aren’t credit-free, but the focus is on the property

- Entity info (if buying through an LLC): Formation documents, EIN, and operating agreement

The big question lenders ask: Will the property’s income cover the mortgage, taxes, insurance, and fees? That’s where the DSCR ratio comes in.

Pro tip: The magic DSCR number is usually 1.0 or higher—meaning the property brings in at least as much as the monthly payments. The higher your ratio, the better your terms.

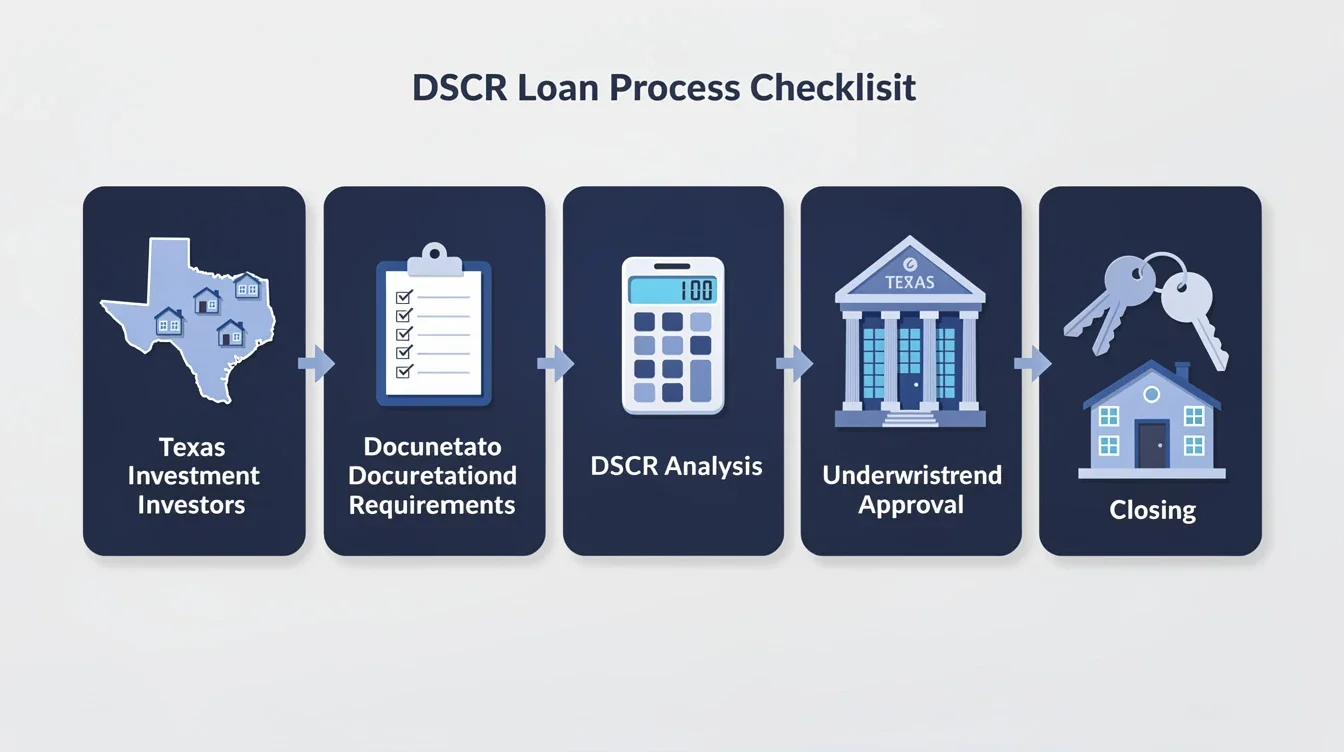

The DSCR Loan Application Process

So you’ve got your paperwork ready and found the perfect Texas investment property. What’s next? Let’s break down the typical DSCR loan process so you know what to expect.

First, you’ll fill out a loan application—either online or with our team’s help. Unlike a traditional mortgage, you don’t need to submit piles of pay stubs or tax returns. Instead, we’ll focus on the property’s numbers.

Next comes the property appraisal. This step is crucial, because the lender wants to confirm the property’s value and rental income potential. We’ll order an appraisal that includes a rent schedule (Form 1007, if you’re curious)—this helps estimate what the property should earn.

Once the appraisal’s in, the underwriting team reviews everything: property income, your credit, and your down payment funds. They’ll calculate the DSCR ratio and decide if the deal checks out.

If all looks good, you’ll get a commitment letter with your loan terms. After that, it’s time to review and sign final documents, wire your down payment, and close the deal. You’ll get the keys and start earning rental income.

Pro tip: Respond quickly to any requests from your lender. The faster you provide info, the smoother and quicker your closing will be.

Key Checklist Items for Texas Investors

Texas is its own world when it comes to real estate. Here’s what you’ll want to pay extra attention to as a Texas investor going for a DSCR loan:

- Property taxes: Texas has higher property taxes than many states. Make sure your projected rental income accounts for this.

- Insurance: Depending on where your property is (think: Gulf Coast, tornado alley), insurance costs can vary. Get accurate quotes.

- HOA fees: If you’re buying a condo or townhome, factor in any homeowners association dues.

- Local rental market: Lenders will look at comparable rents nearby—so do your homework to ensure your numbers are realistic.

At Casey Sullivan Mortgage, we can help you navigate these Texas-specific quirks, because we live and work here, too.

Pro tip: Work with a local real estate agent and property manager who know the Texas market inside and out. Their expertise can boost your approval odds and long-term success.

Common Roadblocks and How to Avoid Them

Even with the best plan, hiccups can happen. Here are some of the most common DSCR loan challenges Texas investors face—and how to sidestep them:

- Low DSCR ratio: If your property’s income isn’t enough, consider boosting rent, putting down a larger down payment, or finding a property with better cash flow.

- Appraisal surprises: Sometimes, the appraised value or estimated rent comes in lower than expected. Stay flexible and have a backup plan—like negotiating price or switching properties.

- Entity complications: If you’re buying through an LLC, make sure all your paperwork is in order, with clear ownership percentages and signatures.

- Timing issues: Real estate moves fast in Texas. Get prequalified early and be ready to move when you find the right property.

Pro tip: Stay in close touch with your lender (that’s us!) throughout the process. We’ll flag any issues early and work with you to find solutions—no last-minute surprises.

Final Steps: Closing and Next Moves

The finish line is in sight! Once you’re cleared to close, you’ll review final loan documents with your closing agent and wire your down payment. After signing on the dotted line, the property officially becomes yours.

From here, you’ll want to:

- Set up your property management (if you’re not handling it yourself)

- Notify tenants or start marketing for new renters

- Keep all loan documents handy for your records

And don’t forget: Your relationship with your lender doesn’t end at closing. The Casey Sullivan Mortgage team is always here to answer questions, help you with future loans, or strategize about growing your portfolio.

Pro tip: Consider checking in with your lender annually to review your investment’s performance and discuss refinancing or expanding when the time is right.

Conclusion

DSCR loans are a powerful tool for Texas investors who want to grow their real estate portfolio without the hassle of proving traditional income. By following this checklist and working with an experienced, service-focused team like Casey Sullivan Mortgage, you’ll turn a complex process into a clear, manageable path to investment success.

Remember, every property and investor is unique—and we’re here to help you every step of the way. Ready to get started? Let’s make your Texas investment dreams a reality, one DSCR loan at a time.