Let’s be real—navigating the mortgage world can feel like a maze, especially if you’re self-employed and have your eyes (and investments) on more than one property. Maybe you’re growing your real estate portfolio in Austin or finally ready to snag that vacation home on the Gulf Coast. Wherever you are in the U. S., the process can feel overwhelming. But here’s the good news: with the right prep and a little expert guidance, qualifying for a mortgage as a self-employed borrower with multiple homes doesn’t have to be a headache.

At Casey Sullivan Mortgage, we’ve helped folks from all walks of life—entrepreneurs, freelancers, investors, and families—secure the keys to their dream homes. If you’re self-employed and looking to buy, refinance, or invest in multiple properties, let’s break down what you need to know, what lenders are really looking for, and how you can put your best foot forward.

Self-Employed?

Here’s What Lenders Really Want

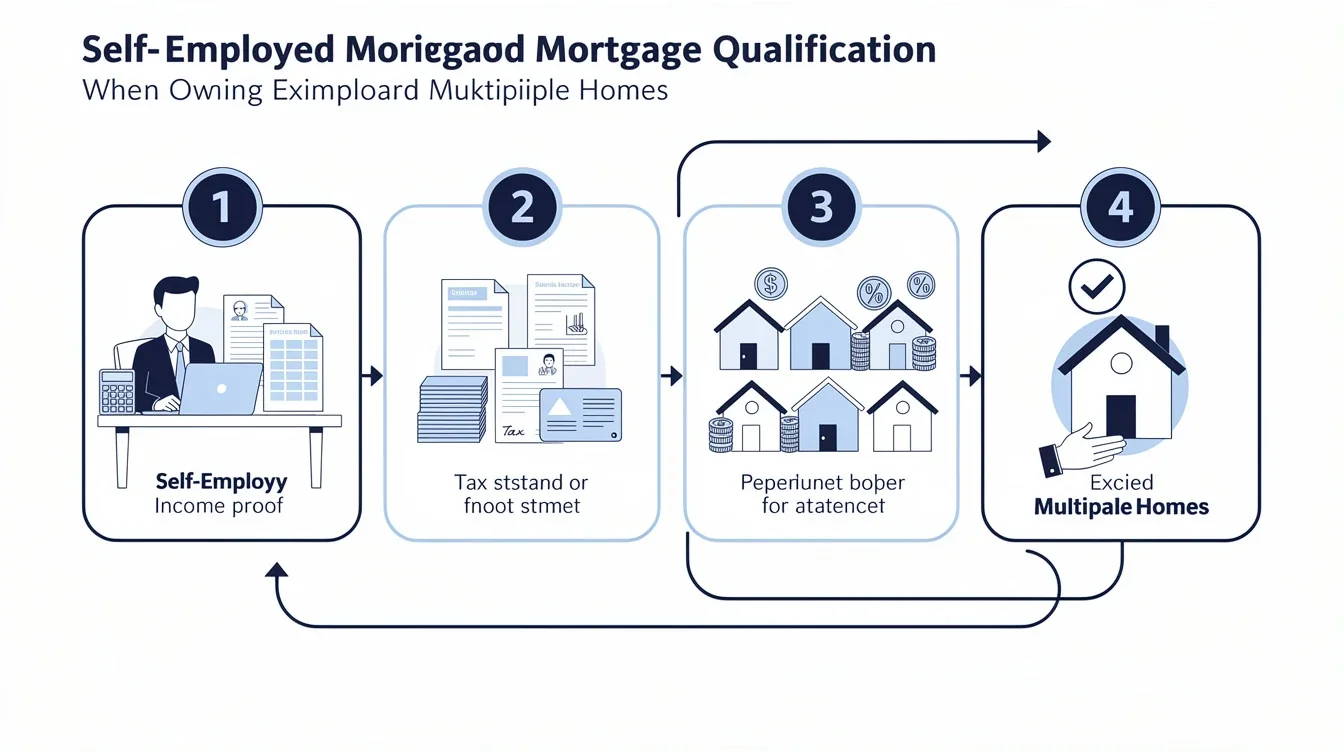

First things first: if you work for yourself, you already know how rewarding—and challenging—it can be. When it comes to mortgages, lenders want to see that your income is reliable, even if it’s not coming in the form of a traditional W-2.

So, what counts as proof? Think two years’ worth of tax returns, profit and loss statements, and sometimes even bank statements. Lenders will look closely at your net income (after expenses), not just your gross revenue. This can be a surprise for those who write off a lot of business expenses.

Pro tip: If you’re planning to apply for a mortgage in the next year or two, it may be worth dialing back on those write-offs. Showing higher net income could make qualifying for a larger loan easier.

Communication is key here. At Casey Sullivan Mortgage, we’ll walk through your documents to gether so there are no surprises. We love helping self-employed borrowers tell the full story behind their numbers—sometimes creativity and context matter more than you think.

Qualifying for Multiple Mortgages

Thinking about your second (or third, or fourth) home? Whether you’re eyeing a rental property, vacation getaway, or a new primary residence, lenders see multiple mortgages as both an opportunity and a risk.

The main concern? Debt-to-income ratio (DTI). Lenders want to be sure you can handle the payments on all your properties without stretching yourself too thin. They’ll weigh your total monthly debts—including all mortgages, property taxes, insurance, car payments, and more—against your income.

If you’re planning to rent out one property, lenders may count a portion of your projected rental income toward your qualifying income. But, they’re often conservative—usually only 75% of rental income gets counted, and you’ll need documentation like a lease agreement.

Pro tip: If you’re buying an investment property, have a clear paper trail for any rental income and be prepared to show reserves—think several months’ worth of mortgage payments saved up just in case.

Don’t worry: multiple mortgages are totally doable. We’ll help you strategize, crunch the numbers, and present a strong application.

Common Challenges—and How to Tackle Them

Let’s be honest: being self-employed and owning several homes means your finances might look a bit more complex. Here are a few roadblocks you might run into, and how we help you overcome them:

1. Variable Income: Maybe your business is seasonal or you had a rough year. Lenders average your income over two years, so a recent dip might lower your qualifying amount. We can help you document any explanations—like a temporary dip due to COVID or a big investment in your business that’s paying off now.

2. Tax Write-Offs: As mentioned earlier, lots of deductions can shrink your qualifying income. Sometimes, we can use bank statement loans or alternative documentation loans, which look at your cash flow rather than just your tax returns.

3. Credit Scores: More mortgages mean your credit is under extra scrutiny. Make sure all your payments are current, avoid big new debts, and keep an eye out for errors on your credit report.

4. Down Payments and Reserves: For investment and second homes, you’ll typically need a larger down payment (often 15-25%) and cash reserves. We’ll help you plan ahead so you’re not scrambling at the last minute.

Pro tip: Start organizing your paperwork early, even if you’re just considering a new purchase. The more time we have, the easier it’ll be to spot and fix any issues.

The Power of Teamwork: Why a Good Mortgage Partner Matters

Let’s face it, the mortgage process is rarely a solo sport—especially when things get complicated. When you work with Casey Sullivan Mortgage, you get a whole team on your side. Here’s what that means for you:

- We’ll review your full financial picture, not just your tax returns. If there’s a story to tell behind your numbers, we’ll help you tell it.

- We’ll communicate with your CPA, financial advisor, or business partners as needed—so you don’t have to play middleman.

- We’ll shop multiple lenders and loan products to find the right fit, whether it’s a conventional loan, jumbo mortgage, or something more creative.

- We’ll keep you updated every step of the way, and make sure you understand your options.

Pro tip: Don’t be shy about sharing your goals. Whether you want to build a rental empire or just find an easier way to juggle your current mortgages, the more we know, the better we can help.

Setting Yourself Up for Success

Ready to get started? Here’s how to put yourself in the best possible position:

- Keep immaculate records. Save your tax returns, profit and loss statements, business licenses, and bank statements. If you’ve got multiple businesses, keep them separated.

- Monitor your credit. Pay bills on time, keep balances low, and don’t open or close accounts right before applying.

- Plan for liquidity. The more cash reserves you have, the better. Lenders want to see that you’ve got a cushion.

- Think ahead. If you’re planning a big move—like buying several properties in the next few years—let’s map out a strategy to gether.

Pro tip: Even if you’re not ready to apply today, a quick check-in with a mortgage pro can help you spot any red flags early, so you’re not caught off guard later.

Conclusion

Being self-employed and managing multiple homes might feel like you’re running a small empire. But with the right preparation and a team that’s got your back, qualifying for a mortgage is totally within reach. At Casey Sullivan Mortgage, we love helping ambitious, entrepreneurial folks like you make the most of every opportunity—whether it’s your first home, your next investment, or that long-awaited vacation retreat.

Don’t let paperwork or process keep you from reaching your real estate goals. With clear guidance, a hands-on approach, and a little teamwork, you can turn those dreams into a reality—no matter how complex your finances might seem. Ready to take the first step? We’re here to help every step of the way.