Thinking about transforming your Texas home? Maybe you’ve been eyeing that fixer-upper in a great neighborhood, or you’re daydreaming about adding a new wing to your current place. Remodeling can be incredibly rewarding, but let’s be honest—it can also be intimidating, especially when it comes to financing the project. That’s where construction to permanent loans come in, and at Casey Sullivan Mortgage, we’re all about making your dreams feel doable. Let’s break down everything you need to know, in plain English, so you can confidently take the next step toward your perfect home.

What Is a Construction to Permanent Loan?

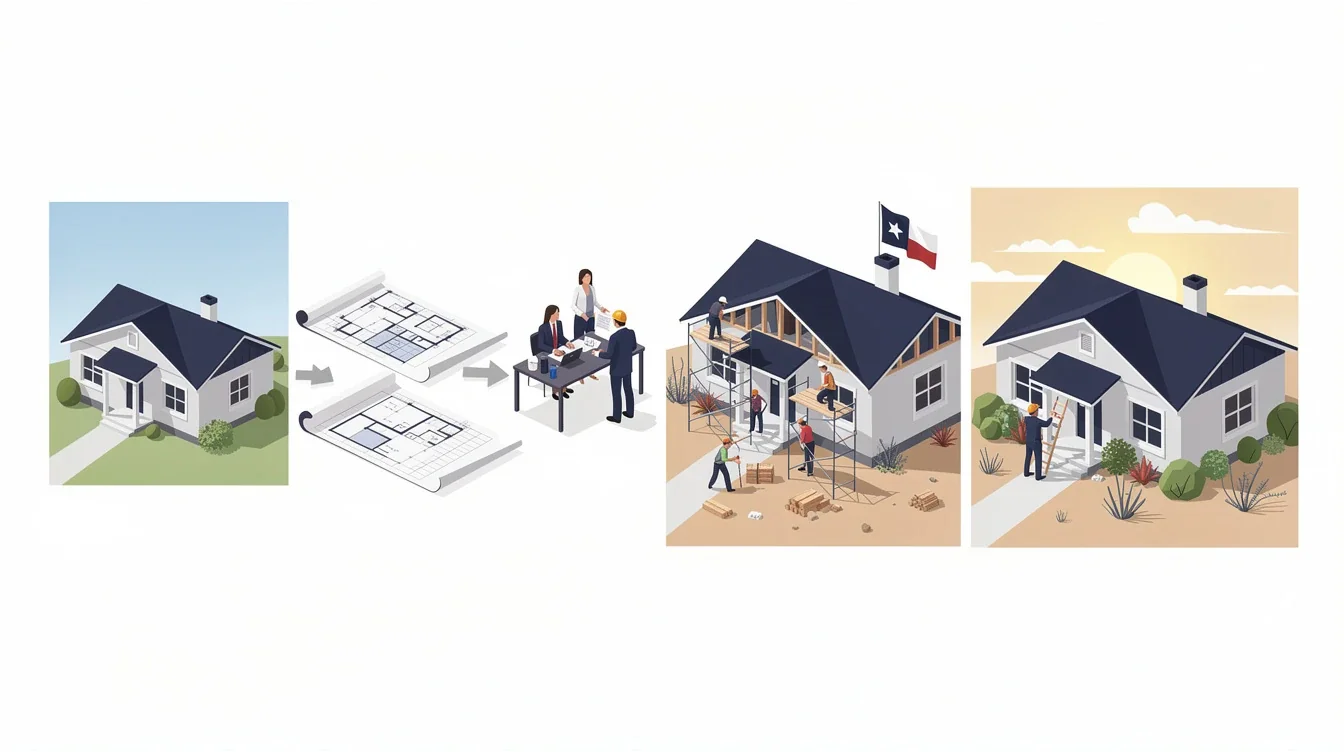

Alright, let’s start with the basics. A construction to permanent loan (sometimes called a “one-time close” loan) is exactly what it sounds like—a single loan that covers both the costs of building (or remodeling) your home and then automatically converts into a standard mortgage when the work’s done.

Why is this a big deal? In the past, you might’ve needed two separate loans: one for the construction phase and another for the mortgage once you moved in. That meant double the paperwork, double the closing costs, and double the hassle. With a construction to permanent loan, you get one streamlined process and one set of closing costs. Easy, right?

Here’s how it works: during construction, you’ll make interest-only payments on the money that’s been drawn out for work that’s completed. Once the remodel is finished and your home is move-in ready, the loan converts to a traditional mortgage, and you’ll start making your regular monthly payments.

Pro tip: If you’re remodeling in Texas, make sure you’re working with a lender who knows the local market. Texas has some unique rules and regulations when it comes to home loans, and you want someone in your corner who speaks the language.

Why Choose a Construction to Permanent Loan for Remodeling?

If you’re planning a major remodel—think adding a second story, gutting your kitchen, or turning a dated ranch into a modern masterpiece—a construction to permanent loan can be a life-saver. Here’s why:

First, it simplifies your life. Instead of juggling multiple loans and lenders, you have one team guiding you from start to finish. That means less stress and fewer surprises.

Second, it’s often more cost-effective. Closing costs can really add up, so only paying them once is a smart move. Plus, you lock in your mortgage rate before construction even begins. That’s huge, especially if you’re worried about rates going up while your remodel is underway.

Third, these loans are designed for big projects. If you’re only painting the walls or swapping out carpet, a traditional cash-out refinance or home equity loan might work better. But for substantial renovations—think structural changes, additions, or down-to-the-studs remodels—a construction to permanent loan gives you the flexibility and funding you need.

Pro tip: Start talking to your lender early. They’ll help you figure out if your project qualifies and walk you through what to expect, so there are no unwelcome surprises down the road.

How the Process Works

Okay, so what’s it actually like to get one of these loans? Let’s walk through the steps to gether:

1. Initial Application: You’ll start by applying for the loan, just like you would with any mortgage. Your lender will want to know about your finances, your remodeling plans, and your contractor.

2. Project Planning: This is where you and your builder (or contractor) create detailed plans and a budget. The more specific, the better—lenders want to know exactly what their money is funding.

3. Appraisal and Approval: The lender will order an appraisal, based on what your home will be worth after the remodel. This “as-completed” value determines how much you can borrow.

4. Closing: Once everything checks out, you’ll close on the loan. This is when the construction loan phase officially begins.

5. Construction Phase: Money isn’t handed over all at once. Instead, funds are released in draws as work is completed. Your lender will inspect the progress before each draw.

6. Conversion to Mortgage: Once the project is finished and passes inspection, your loan automatically converts to a regular mortgage. No need for another closing or mountains of paperwork.

Pro tip: Keep your contractor in the loop from the very beginning. A lender experienced with remodeling loans will help coordinate the process, but having a contractor who knows how draws work and can meet the lender’s documentation requirements is priceless.

What to Know About Texas Remodeling Loans

Texas is a fantastic place to live, but if you’ve looked into home financing before, you know the state marches to the beat of its own drum. There are some unique quirks about construction to permanent loans in Texas you should know about:

Homestead Laws: Texas has some of the strongest homestead protections in the country. That’s great for homeowners, but it means lenders have extra hoops to jump through, especially for cash-out refinances and construction loans tied to your primary residence.

Loan Limits: The maximum loan amount you can get may be affected by county limits or specific lender guidelines. If you’re in a high-cost area or planning a luxury remodel, it’s a good idea to check with your lender early.

Draw Schedules: Texas lenders tend to be pretty strict about how and when funds are released during construction. Expect regular inspections and documentation at each stage. It’s all about protecting you—and the lender—from unfinished work or cost overruns.

Contractor Requirements: Most lenders will want you to use a licensed, insured contractor with a solid track record. If you’re hoping to DIY your remodel, talk to your lender right away—some may allow it, but many do not.

Pro tip: Texas remodeling loans aren’t one-size-fits-all. Working with a local, experienced lender (like the team at Casey Sullivan Mortgage!) can help you avoid common pitfalls and keep your project on track.

Tips for a Smooth Construction to Permanent Loan Experience

Remodeling is a big adventure. To make the process as smooth as possible, here are a few things to keep in mind:

Get Clear on Your Vision: The more detailed your plans, the better. Lenders (and contractors) love specifics—floor plans, material lists, budgets, and timelines. It helps everyone stay on the same page and keeps surprises to a minimum.

Budget for the Unexpected: Even the best-planned remodels can hit a snag or two. Build a little cushion into your budget for contingencies. It’ll save you a lot of stress if something unexpected pops up.

Stay Involved: It’s your home, after all! Stay in touch with your contractor, show up for inspections when you can, and ask lots of questions. The more engaged you are, the happier you’ll be with the end result.

Work With the Right Team: Not every lender is experienced with construction to permanent loans or Texas’s unique rules. Look for a mortgage team that’s done this before and treats you like a partner, not just a file number.

Pro tip: Don’t be afraid to ask for references! A good contractor or lender will be happy to connect you with past clients who can share their experiences.

Common Questions About Remodeling Loans

If you’ve never tackled a big remodel before, it’s normal to have lots of questions. Here are a few of the ones we hear most often:

How much can I borrow with a construction to permanent loan?

It depends on your income, credit, the value of your home after the remodel, and local loan limits. Your lender will help you crunch the numbers.

Will I need a big down payment?

Usually, you’ll need at least 10-20% down based on the total cost of the project (including both land and construction, if you’re building from scratch).

Do I have to move out during construction?

It depends on the scope of your remodel. For big projects, you might need to find temporary housing, especially if your kitchen or bathrooms will be out of commission.

What if my project goes over budget?

Try to plan as accurately as possible up front, but if you run into overages, talk to your lender right away. Sometimes, you can modify your loan, but it’s better to build in a cushion from the start.

Can I use a construction to permanent loan for investment properties or vacation homes?

Yes, though the process and requirements can be a little different than for a primary residence. Let your lender know your plans so they can guide you accordingly.

Pro tip: There’s no such thing as a dumb question. Your lender should be your partner throughout this process, so don’t hesitate to reach out any time you need clarity.

Conclusion

Remodeling your Texas home is a big deal, but with a construction to permanent loan, it doesn’t have to be overwhelming. At Casey Sullivan Mortgage, we’re all about helping you turn your house into the home you’ve always wanted—without the stress, confusion, or endless paperwork. If you’re ready to take the next step, let’s chat. We’ll answer your questions, walk you through the process, and make sure you have a team in your corner every step of the way. Here’s to making your dream home a reality!